Nourishing Resilience: Adapting Food Systems for Climate Realities

Eric Desai — November 1, 2024

“Adaptability has been an essential ingredient for surviving and thriving for every species of life, from life’s beginning on Earth.” –Ronald Heifetz, Marty Linksy

If you have glanced at your grocery bill lately, you probably felt a sense of disbelief—the prices have almost doubled what they were a year ago. As you navigate the aisles, the stark reality of rising food prices hits you at every turn.

That bottle of olive oil you use for cooking? Its price has nearly doubled compared to two years ago. Your favorite brand of coffee? The price has jumped by a quarter within the last 12 months alone, making your daily brew feel like a luxury.

As you unpack your groceries, you may wonder if this is the new normal. Rising prices are causing many to rethink their choices, such as opting for cheaper brands, purchasing smaller quantities, or changing their favorite recipes. These are not just numbers on a receipt; they are shifting the way we eat, shop, and live.

While various factors contribute to rising food costs, climate change is becoming one of the most significant. Brazil, the world’s top coffee producer, is enduring its worst drought in 70 years, slashing yields and driving up prices worldwide. At the same time, the U.S. Southeast is reeling from Hurricane Helene, a catastrophic storm that has taken hundreds of lives, left millions without power and caused an estimated $160 billion in damages, including $7 billion in crop losses alone.

These events reveal the fragility of our interconnected food systems. As climate disruptions become more frequent and severe, harvests will suffer, growing seasons will shift, and agricultural regions will be transformed. This won’t just drive food price instability; it will create broader challenges that ripple across the entire food value chain, affecting stakeholders—from producers to consumers—at every level.

At GroundForce Capital, we recognize the profound impact climate change has not only on the broader economy but also on global food production and distribution. We invest across the entire consumer packaged goods (CPG) value chain, from agricultural innovation to beloved consumer brands, actively shaping the future of our food system*.

Our portfolio companies, like much of the food industry*, are tackling the operational challenges posed by shifting climate patterns, including supply chain disruptions, inflation of critical commodities, and compressed profit margins. These challenges are exacerbated by the concentration of agricultural production, both geographically and by crop type, which creates vulnerabilities in our food system. While this concentration can be economically efficient in stable times, it risks significant vulnerabilities in an era of climate variability, leading to more frequent supply disruptions and price volatility in the global food market.

For all participants in the food value chain, this reality presents both challenges and opportunities. While much of the climate discourse has focused on mitigating greenhouse gas emissions, we believe that adaptation is equally crucial. Adapting food systems involves adjusting practices, processes, and infrastructure to reduce vulnerability to climate impacts. By embracing this approach, we can build food systems that are not only more sustainable but also resilient, capable of thriving amidst ongoing climate changes. At GroundForce Capital, we are committed to investing in and supporting the innovations that will make this vision a reality.

*Authors’ Note: While this article focuses primarily on the food system, many of the impacts and insights discussed are also applicable to the broader food, beverage, and consumer packaged goods (CPG) industries.

A Climate-Disrupted Food System

The impacts of climate change on global food systems are multifaceted and interconnected. Climate change is reshaping our food systems in several critical ways:

Shifting Temperature Zones

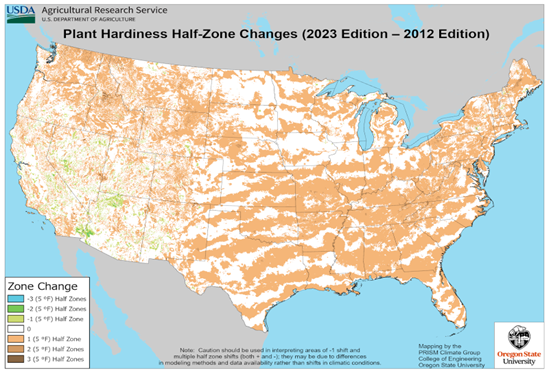

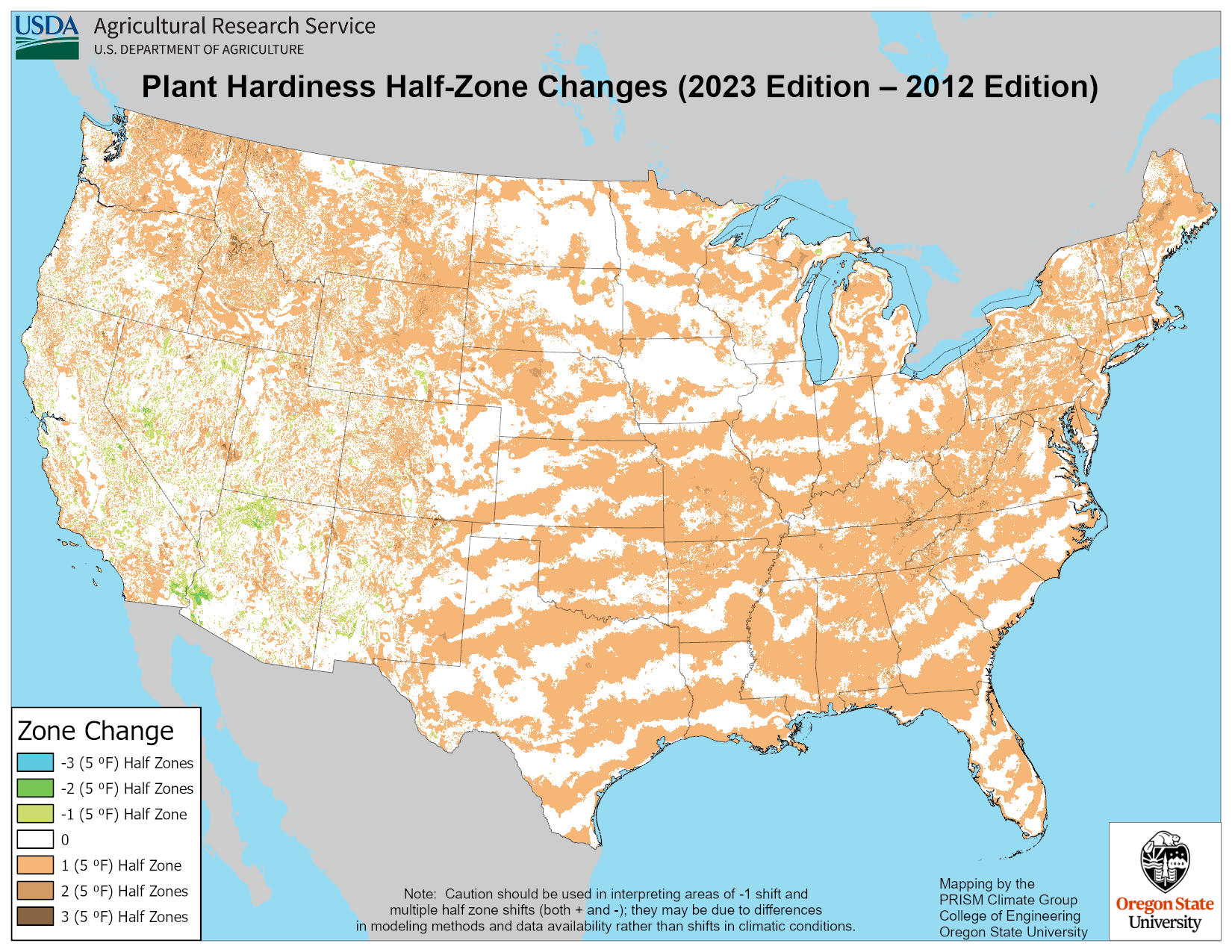

Global temperature increases are already causing significant alterations in traditional growing regions worldwide. This is exemplified by changes in temperature classification systems like the United States Department of Agriculture’s (USDA) Plant Hardiness Zones. These zones, which guide farmers on suitable crops for their area, have shifted notably in recent years. Over the past decade alone, these zones have moved northward by half a zone—equivalent to a 5°F increase in average annual minimum temperatures.

USDA Plant Hardiness Zone Map comparison 2012 vs. 2023 (Source: USDA).

Similar shifts are being observed globally, impacting agricultural production and commodity prices. For instance, in 2020, France experienced a 27% decrease in wine production due to record-breaking heat, while a 2021 heatwave in the state of Washington destroyed 30% of its cherry crop, resulting in $100 million in losses, with some farmers reporting cherries melting off the trees.

Looking forward, research projects these zones will continue to move northward at a rate of approximately 20–60 km per decade, dramatically reshaping the agricultural landscape. For example, by the end of the century, suitable areas for olive cultivation in Spain could decrease by 22% to 72%, while some varieties could be wiped out entirely. This would drastically disrupt the global olive oil market, as Spain currently produces about 40% of the world’s supply.

Changing Precipitation Patterns

Climate change is driving substantial alterations in global rainfall patterns as certain regions are experiencing increased precipitation and flooding, while others face prolonged periods of drought. In 2021, Brazil experienced its worst drought in nearly a century, coupled with a severe frost, causing coffee prices to increase as much as 60%. A year later, Pakistan’s floods destroyed over 3.6 million acres of crops, wiping out 80% of rice crop and 70% of cotton fields in some regions, equating to $3.7 billion in agricultural and livestock losses.

One of the millions of farmers that were impacted by the severe floods in Pakistan (Source: NY Times).

These unpredictable shifts in precipitation introduce significant volatility, making agricultural planning increasingly difficult. California serves as a prime example of this challenge: a decade ago, droughts between 2014 and 2016 caused $3.8 billion in agricultural losses, followed by a severe flood the following year that inflicted millions in additional damage. Recent droughts have also forced many farmers to remove or abandon almond orchards, altering long-term production capacity.

Extreme Weather Events

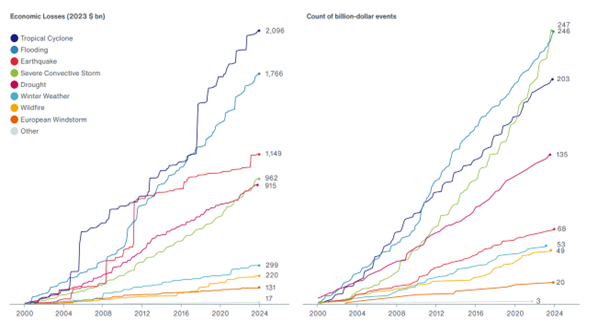

Climate change is amplifying both the frequency and severity of extreme weather events, posing significant challenges to global food systems. According to the World Meteorological Organization, weather-related disasters have increased fivefold over the past 50 years, with economic losses rising sevenfold. Extreme weather events like hurricanes, floods, and wildfires, which are expected to become even more frequent, threaten to devastate crops and disrupt supply chains on a massive scale.

Cumulative global economic losses have accumulated to over $2 trillion since 2000 (Source: Aon).

Recent events highlight the severity of these impacts: in 2017, Hurricane Maria destroyed 80% of Puerto Rico’s crop value, causing roughly $1 billion in agricultural losses. Similarly, California’s 2018 Camp Fire devastated 30,000 to 40,000 acres of rangeland in Butte County, displacing animals and severely affecting grazing land for livestock.

Locomoting Tides for Food System Stakeholders

Climate change is reshaping the entire food system, affecting stakeholders at every level of the supply chain. The consequences are far-reaching, from production challenges to shifting consumer behaviors.

Upstream Input Producers: Companies producing agricultural inputs are highly sensitive to energy market volatility, exacerbated by climate change. Extreme weather events can disrupt energy production and distribution, leading to price fluctuations.

This volatility is amplified by geopolitical events, as demonstrated by the Russia-Ukraine conflict, which caused a surge in natural gas prices—a key component in fertilizer production. Additionally, unpredictable weather patterns complicate decisions about effective inputs for upcoming growing seasons. These factors create a ripple effect of increased costs and uncertainty throughout the food supply chain, impacting farmers and consumers alike.

Farmers: Positioned on the front lines of our changing food system, farmers face mounting challenges that threaten their production, financial stability, and livelihoods. Extreme weather events, such as the 2019 Midwest floods that prevented 19.4 million acres of crops from being planted, are growing more frequent. Rising temperatures and unpredictable weather patterns are exposing outdoor workers to heightened heat stress, reducing labor capacity during critical periods. Livestock is also vulnerable, experiencing decreased fertility, health complications, and reduced production due to heat stress. Additionally, climate change is altering the distribution of pests, weeds, and diseases in agricultural systems, increasing biotic stress on crops and livestock. Small-scale farmers, who often lack access to crop insurance and advanced technologies, are especially vulnerable to these challenges.

Fishers and Aquaculture Operators: Climate change is significantly altering marine and freshwater ecosystems. Ocean warming has decreased the sustainable yields of some wild fish populations, forcing fishers to travel farther or shift their target species.

Additionally, ocean acidification and rising temperatures are already affecting farmed aquatic species, further complicating aquaculture operations. Small-scale and artisanal fishers in tropical regions, who often lack the resources to adapt quickly, are especially vulnerable to these shifts. As climate change alters marine ecosystems, it threatens not only livelihoods but also the food security of coastal communities and beyond.

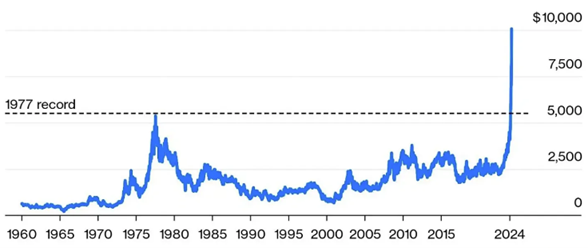

Food Manufacturers and Processors: These stakeholders are grappling with rising commodity prices, supply chain disruptions, and resource scarcity. For example, cocoa prices have nearly tripled this year due to climate-related disruptions in West Africa, which accounts for 70% of global supply.

As a result, companies like Hershey are exploring alternative ingredients, adjusting their product offerings, and diversifying their supply chains. Water scarcity is also forcing companies to rethink their resource use and help support municipal infrastructure in water-stressed regions.

Additionally, climate change is significantly impacting food safety as higher temperatures and humidity accelerate the growth of toxigenic fungi, plant and animal-based pathogens, and harmful algal blooms. More frequent and severe flooding is expected to further increase the risk of food contamination.

Cocoa prices have surged to more than $10,000 per metric ton (Source: Bloomberg).

Distributors and Retailers: Shifting climates are complicating food storage and transportation, exposing vulnerabilities in complex supply chains. Rising temperatures increase the need for refrigeration, driving up both costs and emissions for distributors and retailers.

Extreme weather events frequently disrupt transportation routes, further increasing freight costs. Grocers face climate-induced supply volatility, complicating procurement strategies. At the same time, they are under growing pressure to reduce food waste and improve sustainability efforts, further squeezing already thin profit margins.

Consumers: The impacts of climate change are becoming increasingly evident on supermarket shelves and household budgets worldwide. Prices for essential goods like coffee, dairy, fruit, eggs, and cooking oils have surged partly due to climate-related factors.

For example, olive oil prices have doubled over the past year, primarily due to severe droughts and heat in major producing regions like Spain, while orange juice costs have doubled since 2020, driven by extreme weather and citrus diseases affecting Florida’s crop yields.

These effects also extend to household goods like laundry detergent and personal care products, many of which rely on agricultural ingredients. As raw material costs rise, consumers will see increased prices for these everyday items, further straining family budgets.

These price hikes disproportionately impact vulnerable groups, including women, children, low-income households, Indigenous communities, and small-scale producers. The consequences extend beyond immediate financial strain, as food insecurity can lead to long-term health issues and reduced educational outcomes.

In urban areas, particularly in low-income neighborhoods, climate change exacerbates the problem of food deserts—areas with limited access to affordable, nutritious food. As extreme weather events disrupt supply chains and drive up food prices, these areas become even more vulnerable, further widening the nutrition gap between affluent and disadvantaged communities.

The impact of climate change on food security extends beyond individual households and local communities. The World Bank projects that climate change could push an additional 132 million people into poverty by 2030, driven largely by escalating food costs and declining agricultural yields.

Furthermore, climate change is increasingly driving migration, as people are forced to leave areas where agricultural productivity has declined or where extreme weather events have made living conditions untenable. This climate-induced migration often exacerbates existing food security challenges, both in the regions people are leaving and, in the areas where they resettle, creating a complex web of interconnected global issues.

Policymakers: These stakeholders play a pivotal role in driving climate adaptation across food systems. To improve resilience, policymakers can implement financial incentives for regenerative agriculture, develop stricter environmental standards, and invest in climate-resilient crops and technologies. They can also enhance disaster preparedness, strengthen social safety nets for affected farmers, and support climate-resilient infrastructure. These measures are vital not only for food security but also for maintaining geopolitical stability, as food insecurity can lead to social unrest and political instability.

Additionally, climate adaptation policies tend to be less partisan and more politically agnostic, making them easier to implement across different administrations. While steps have been taken, such as the U.S. Bipartisan Infrastructure Law, which allocated billions for climate resilience projects, and the EU’s Corporate Sustainability Reporting Directive, more comprehensive action is crucial. Policies must evolve rapidly to keep pace with climate change, particularly in vulnerable regions where food security is at risk.

Across the food system, stakeholders are facing rising operational costs, supply chain uncertainties, and the need for long-term strategic shifts.

These pressures are pushing all players to strengthen their ability to measure, monitor, report, and manage climate-related risks.

The interconnectedness of these challenges underscores the need for a collaborative, system-wide approach to building resilience in our food systems, requiring coordinated efforts from the private sector, governments, and civil society organizations.

Complementing Mitigation with Resilience

“If decarbonization is the new industrialization, adaptation is the new modernization.” – The CleanTech Group

Effective climate change strategies require both mitigation and adaptation efforts, each playing a crucial role in addressing the challenges ahead. While mitigation focuses on reducing greenhouse gas emissions to slow the pace of climate change, adaptation is about modernizing our systems and infrastructure to withstand and thrive in the face of climate impacts that are already being felt.

Why is adaptation so vital? Even if we halted all greenhouse gas emissions today, we would still face decades of climate change due to the gases already in the atmosphere. Therefore, adaptation is not an alternative to mitigation but a necessary complement to it. In the food system, adaptation refers to adjusting agricultural practices, supply chain processes, and production infrastructure to strengthen resilience against climate-related risks.

In many cases, adaptation strategies can reinforce mitigation efforts, yielding both short-term and long-term benefits. For instance, in the food system, reducing food waste not only strengthens agricultural sustainability (adaptation) but also cuts methane emissions (mitigation). Similarly, protecting forests as part of wildfire management both builds resilience against future climate events and supports decarbonization by preserving natural carbon sinks.

The Strategic Value of Climate Adaptation

The value of climate adaptation is increasingly clear. According to projections by Bank of America, the market for climate adaptation could reach $2 trillion annually within the next five years. However, there remains a significant gap between the need for adaptation and current investment levels. Currently, only 7% of climate-related investments are directed towards adaptation. Even more striking–a mere $43 billion, or 3% of the $1.3 trillion in climate finance spent in 2021 and 2022 was allocated to agriculture, forestry, land use, and fisheries.

Financing climate adaptation is a significant opportunity, not a burden. For every dollar a company invests in adaptation and resilience measures, it can yield $2 to $15 in financial benefits. First movers in the private sector will enjoy a distinct advantage in capturing market share, while those who fail to act may face increased risks: rising operational costs from raw material price surges, diminished revenue from decreased production efficiency, unforeseen asset damage, and higher insurance premiums.

This disparity presents a substantial opportunity for forward-thinking investors across strategies—venture, growth, infrastructure, and development funds. Existing venture funds focused on adaptation and resilience, such as Tailwind, SJF, and Buoyant, have already mapped out the broader space, highlighting the potential for impactful investments.

Adaptation investments for venture and growth investors can possess (but not in all cases, e.g., infrastructure projects) attractive characteristics that make them compelling near-term opportunities, including lower capital expenditures, improved risk-adjusted returns, and accelerated payback periods.

Recent exits of growth-stage companies highlight the potential for strong returns in the adaptation space:

- Constellation Cold Logistics: Acquired by EQT in June 2024, this leading provider of temperature-controlled storage infrastructure supports food producers across Europe. Its facilities help preserve perishable goods, enabling adaptation to rising temperatures and increasing supply chain instability.

- Optimity: Acquired by RELEX Solutions in January 2024, Optimity offers supply chain planning and optimization services for consumer goods companies, helping them adapt to evolving market conditions and climate-related disruptions.

- BIOTROP: Aqua Capital and GIC exited BIOTROP in September 2023 to Biobest for $570 million. The company develops biological inputs for sustainable crop protection and nutrition, aiding farmers in adapting to shifting climates, changing pest pressures, and soil conditions.

- The Climate Service: Acquired by S&P Global in January 2022, this climate risk analytics provider helps corporates and investors assess both physical and transition climate risks. Its tools aid in quantifying climate risks in financial terms, aiding businesses in adapting to climate change and regulatory shifts.

- FoodChain ID: Acquired by Berkshire Partners in December 2020, FoodChain ID provides testing, certification, and inspection solutions for food quality. Its services help food manufacturers and processors adapt to changing safety risks and regulatory environments influenced by climate change.

- Rivulis: Acquired by Temasek in December 2020, Rivulis is a global leader in micro-irrigation solutions, supporting sustainable agricultural practices. Its technologies help farmers increase crop yield while conserving water, addressing climate resilience through precision irrigation and digital farming solutions.

Key Areas of Opportunity in Food System Adaptation

Within an evolving landscape of climate challenges and food security concerns, GroundForce Capital has identified several key areas where technology and innovation can address the pressing issues in our food systems.

These are categories where we see real, scalable solutions focusing on enhancing resilience, optimizing resource use, improving operational efficiency, reducing key business risk, and unlocking new value streams while presenting the opportunity to drive significant societal and investment returns.

Enhancing Agricultural Resilience

- Diversifying crop varieties and implementing regenerative agriculture practices to reduce climate risk and enhance soil health.

- Utilizing precision agriculture technologies, including IoT sensors, drones, and AI, to optimize water usage and predict crop health issues.

- Implementing vertical farming and controlled-environment agriculture to reduce vulnerability to outdoor climate conditions and optimize resource use.

Improving Water Management

- Developing drought-resistant crop varieties and farming techniques to maintain productivity with reduced water usage, particularly in areas facing increasing water scarcity.

- Implementing water-saving technologies such as efficient irrigation systems and water leak detection tools throughout the agricultural and manufacturing supply chain to improve water availability in water-stressed regions.

- Investing in water recycling and treatment technologies for processing facilities, reducing water consumption and dependence on freshwater sources.

Building Resilient Infrastructure

- Implementing smart cold chain solutions to maintain food quality during transport and storage in variable climate conditions.

- Adopting renewable energy solutions and microgrids, such as solar-powered cold storage and localized power systems, to reduce emissions and ensure energy reliability for critical food infrastructure during grid disruptions.

- Investing in advanced food preservation technologies to extend self-life and reduce vulnerability to supply chain disruptions.

Optimizing Supply Chain & Distribution

- Utilizing advanced predictive analytics to anticipate climate-related disruptions and enable proactive supply chain management.

- Building local and regional food systems to shorten supply chains and reduce exposure to global disruptions.

- Deploying AI-powered inventory management systems to optimize stock levels and adapt to climate-induced supply fluctuations.

Enhancing Climate Risk Management & Decision-Making

- Developing advanced climate risk assessment tools for the food and agriculture sector, incorporating big data and AI for more accurate predictions.

- Creating innovative insurance (e.g., parametric insurance) and financial products (e.g., resilience credits) to help farmers and food businesses manage climate-related risks more effectively.

- Utilizing digital twins for food supply chains to simulate and optimize responses to various climate scenarios and implementing early warning systems to mitigate the impact of extreme weather events on production and distribution.

Seeding Solutions, Cultivating Prosperity

The era of climate-driven disruption in our food systems is here, driven by decades of unsustainable practices compounded by anthropogenic climate change and an increasingly complex global supply chain. While extreme weather and its effects on food systems are inevitable, a complete collapse is not – provided we take bold and decisive action.

Addressing this reality requires concerted efforts across the entire food value chain. It demands foresight, creativity, innovation, and a fundamental reimagining of how we grow, process, distribute, and consume food. This is not just an essential response to a more volatile world, but an unprecedented opportunity to redefine the relationship between our food systems and the natural world.

GroundForce Capital is uniquely positioned to support this critical transformation by identifying and investing in innovative solutions that address the impact of climate change on our food systems. With our strong connections across the entire ecosystem—from producers and distributors to retailers and CPG companies—we act as a bridge, enabling comprehensive, holistic solutions. Now is the time for reimagining our food systems. By investing in climate adaptation today, we can ensure a resilient and sustainable food supply for tomorrow and foster a more equitable future for all.

About the Authors: This article was written by Eric Desai, Partner at GroundForce Capital, where he leads technology and services growth investments across supply chain management, agtech, foodtech, manufacturing, resource management, and circularity. Special thanks to David Heifitz, our MBA Investment Fellow, who contributed valuable insights to this piece.

Are you driving meaningful change in these sectors? Whether you are a company demonstrating real impact at scale or an investor passionate about transforming consumer value chains, we would love to connect.

Reach out to eric@groundforcecapital.com to explore opportunities for collaboration and to help shape a more resilient and sustainable future together.

{kind=link}